It’s time to discuss the most disgusting part of borrowing money. That ugly, creeping, lurking, accruing, hunk of junk called interest. The words I’d really like to use to describe how I feel about interest aren’t appropriate for this family-friendly blog. So... use your imagination.

But – before we dive into interest, I’ll share my update! That’s of more interest to you, right?

But – before we dive into interest, I’ll share my update! That’s of more interest to you, right?

November = $832.90

Which brings my total put toward debt since January 1, 2015 to…

Which brings my total put toward debt since January 1, 2015 to…

$15,160.73

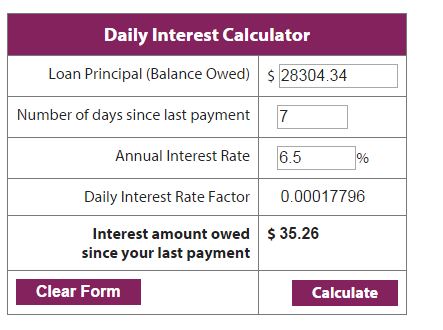

My interest accrues at a rate of 6.5% which is just over $35.25 a week

My interest accrues at a rate of 6.5% which is just over $35.25 a week At the time of this writing, my remaining balance sits at $28,304.34. It will drop into $27K before 2016. While that’s still an overwhelming balance, I feel much better about that number now versus a year ago and have more hope that I will see a balance of $00.00 in the nearer future.

Back to the big, bad, bully of loans and credit.

I get it. Interest is a necessary part of borrowing money. If we didn’t’ have interest, there wouldn’t be lending institutes. There wouldn’t be a way for them to operate. People also wouldn’t have any interest in paying off debts. What I can’t wrap my head around, however, is the interest rate of my loans -- and the restriction I have as a borrower.

All of my student loans are through the government and they each have an interest rate of 6.5%!!! Each day, my remaining balance grows by 6.5%, which translates to just over $5 a day, or $1,839.78 in a year! That's about 2.5 month's worth of debt-dumping efforts!

Those who took out student loans with the government in the same years I did (2006-12) likely have similar rates. People get car loans and mortgages for much lower rates. For example, our mortgage rate is 3.5%. With a car or home loan, borrowers have the ability to refinance. Not so with student loans.

What’s a borrower to do? At this stage in my debt repayment, there are 2 main things.

1. Pay down the principal loan amount as fast as possible. That’s why I embarked on this Fa$t, and why I started making more frequent payments.

2. Use Auto Pay. My lender offers me a small break – 0.25% break, to be exact – on my interest for being enrolled in auto pay. Other lenders may extend this same offer.

There is a third, lesser-known, less-conventional, and...riskier option.

I discovered this option while reading about the adventures of Stephanie and her family on her blog called www.sixfiguresunder.com. She's another Debt Dumper. I mentioned her back in May when I talked about homemade laundry soap.

Stephanie has a post titled "An Unconventional Way to Save Money on Student Loan Interest" in which she talks about how she and her husband have used credit card balance transfers to pay off portions of their student loan debt.

How it works is you apply and get approved for a balance transfer, or loan, through a credit card company. They'll assess your credit and give you a maximum amount, but ultimately, you decide how much to transfer. Then, the credit card company sends you a card loaded with the amount. You use it to pay your student loans, and then work to pay off the card.

Stephanie from Six Figures Under advises (and I agree!) that you do this only if the offer has 0% interest for an extended period (at least a year), and if there aren't any transfer fees. If you pay off the card balance before interest kicks in, you've saved yourself from paying the high interest rates of student loans. You've outsmarted the most disgusting part of borrowing money!

Balance transfers aren't for everyone. You'll want to have the balance transfer paid in full before interest kicks in, otherwise you'll pay interest that's likely triple the rate of student loan interest.

It's best if you're near the end of a loan, i.e., can dump it completely in a year. It's also best if you have a history of making payments on time, consistent income, and responsible money management (ahem...no impulse purchases!).

This proved to be a great option for Novio -- and he did it!

Novio did the transfer in October and has 17 months to pay off the balance (until June 2017) before interest begins accruing. We're anticipating he'll have it paid off a few months prior.

He had $4,993.00 remaining on his student loan repayment. We looked into options and found several that were 0% interest rate, but couldn't find one that did not have balance transfer fees. The card Novio went with had a transfer fee of $5 or 3%, whichever is greater.

In his case, 3% added $149.00. Novio's student loan interest rate is 4.5%, which means he'd pay $224.70 in interest over a year. By doing the balance transfer, he saved himself about $75. Not a huge savings, but savings nonetheless! Had we known about balance transfers sooner, he would have signed on earlier and saved himself more.

I'm considering doing a balance transfer to wipe out a chunk of my remaining balance, say $5K. It's a risk, though. I'll be responsible for making a payment to the credit card, plus continuing to pay my lender an aggressive amount.

What do you think? Have you ever used a balance transfer? Would you consider doing it?

Back to the big, bad, bully of loans and credit.

I get it. Interest is a necessary part of borrowing money. If we didn’t’ have interest, there wouldn’t be lending institutes. There wouldn’t be a way for them to operate. People also wouldn’t have any interest in paying off debts. What I can’t wrap my head around, however, is the interest rate of my loans -- and the restriction I have as a borrower.

All of my student loans are through the government and they each have an interest rate of 6.5%!!! Each day, my remaining balance grows by 6.5%, which translates to just over $5 a day, or $1,839.78 in a year! That's about 2.5 month's worth of debt-dumping efforts!

Those who took out student loans with the government in the same years I did (2006-12) likely have similar rates. People get car loans and mortgages for much lower rates. For example, our mortgage rate is 3.5%. With a car or home loan, borrowers have the ability to refinance. Not so with student loans.

What’s a borrower to do? At this stage in my debt repayment, there are 2 main things.

1. Pay down the principal loan amount as fast as possible. That’s why I embarked on this Fa$t, and why I started making more frequent payments.

2. Use Auto Pay. My lender offers me a small break – 0.25% break, to be exact – on my interest for being enrolled in auto pay. Other lenders may extend this same offer.

There is a third, lesser-known, less-conventional, and...riskier option.

I discovered this option while reading about the adventures of Stephanie and her family on her blog called www.sixfiguresunder.com. She's another Debt Dumper. I mentioned her back in May when I talked about homemade laundry soap.

Stephanie has a post titled "An Unconventional Way to Save Money on Student Loan Interest" in which she talks about how she and her husband have used credit card balance transfers to pay off portions of their student loan debt.

How it works is you apply and get approved for a balance transfer, or loan, through a credit card company. They'll assess your credit and give you a maximum amount, but ultimately, you decide how much to transfer. Then, the credit card company sends you a card loaded with the amount. You use it to pay your student loans, and then work to pay off the card.

Stephanie from Six Figures Under advises (and I agree!) that you do this only if the offer has 0% interest for an extended period (at least a year), and if there aren't any transfer fees. If you pay off the card balance before interest kicks in, you've saved yourself from paying the high interest rates of student loans. You've outsmarted the most disgusting part of borrowing money!

Balance transfers aren't for everyone. You'll want to have the balance transfer paid in full before interest kicks in, otherwise you'll pay interest that's likely triple the rate of student loan interest.

It's best if you're near the end of a loan, i.e., can dump it completely in a year. It's also best if you have a history of making payments on time, consistent income, and responsible money management (ahem...no impulse purchases!).

This proved to be a great option for Novio -- and he did it!

Novio did the transfer in October and has 17 months to pay off the balance (until June 2017) before interest begins accruing. We're anticipating he'll have it paid off a few months prior.

He had $4,993.00 remaining on his student loan repayment. We looked into options and found several that were 0% interest rate, but couldn't find one that did not have balance transfer fees. The card Novio went with had a transfer fee of $5 or 3%, whichever is greater.

In his case, 3% added $149.00. Novio's student loan interest rate is 4.5%, which means he'd pay $224.70 in interest over a year. By doing the balance transfer, he saved himself about $75. Not a huge savings, but savings nonetheless! Had we known about balance transfers sooner, he would have signed on earlier and saved himself more.

I'm considering doing a balance transfer to wipe out a chunk of my remaining balance, say $5K. It's a risk, though. I'll be responsible for making a payment to the credit card, plus continuing to pay my lender an aggressive amount.

What do you think? Have you ever used a balance transfer? Would you consider doing it?

RSS Feed

RSS Feed